Documenting my journey operating a $500 million self storage portfolio & running multiple real estate, and real estate technology companies with 60 employees.

Storage in 2024

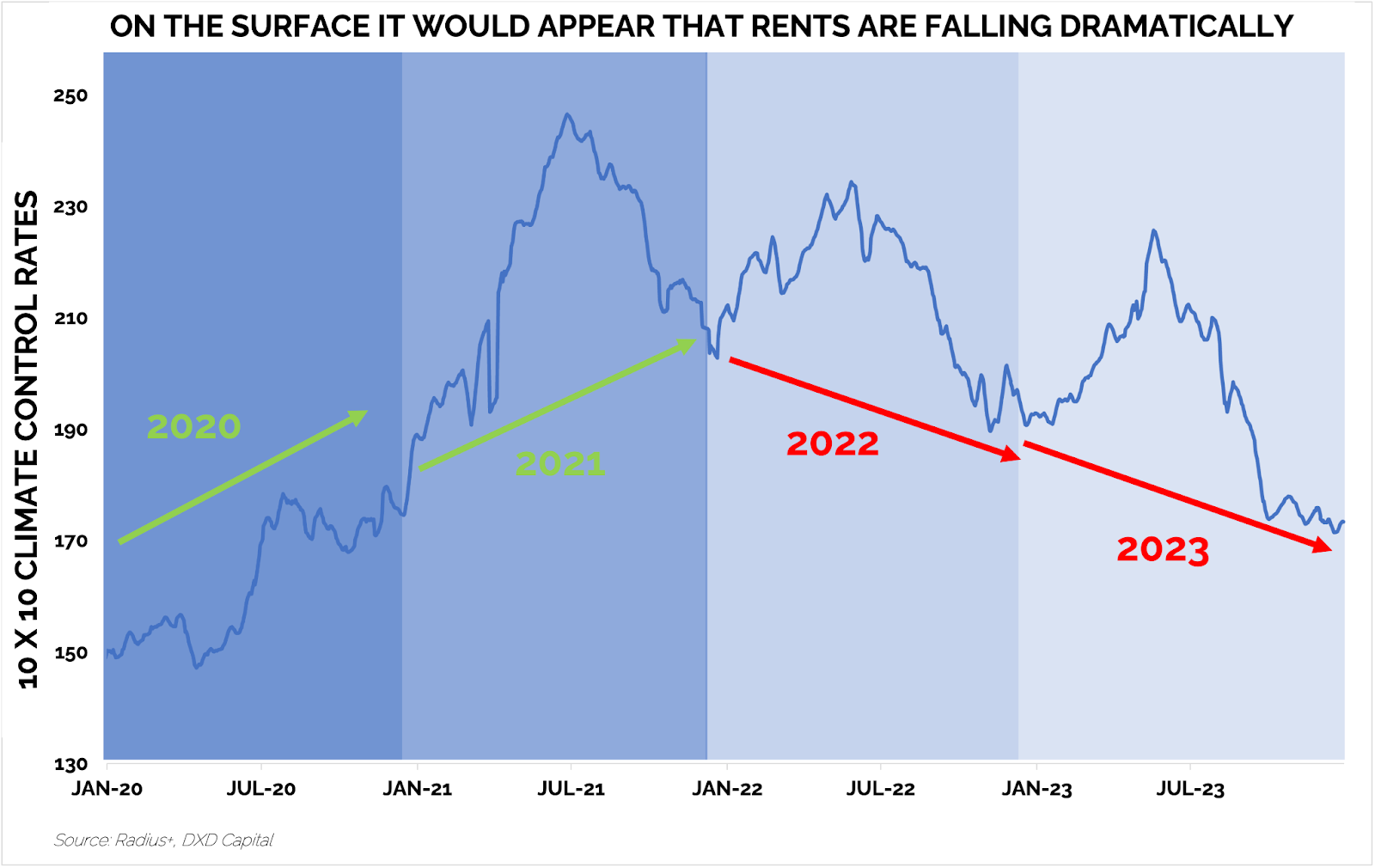

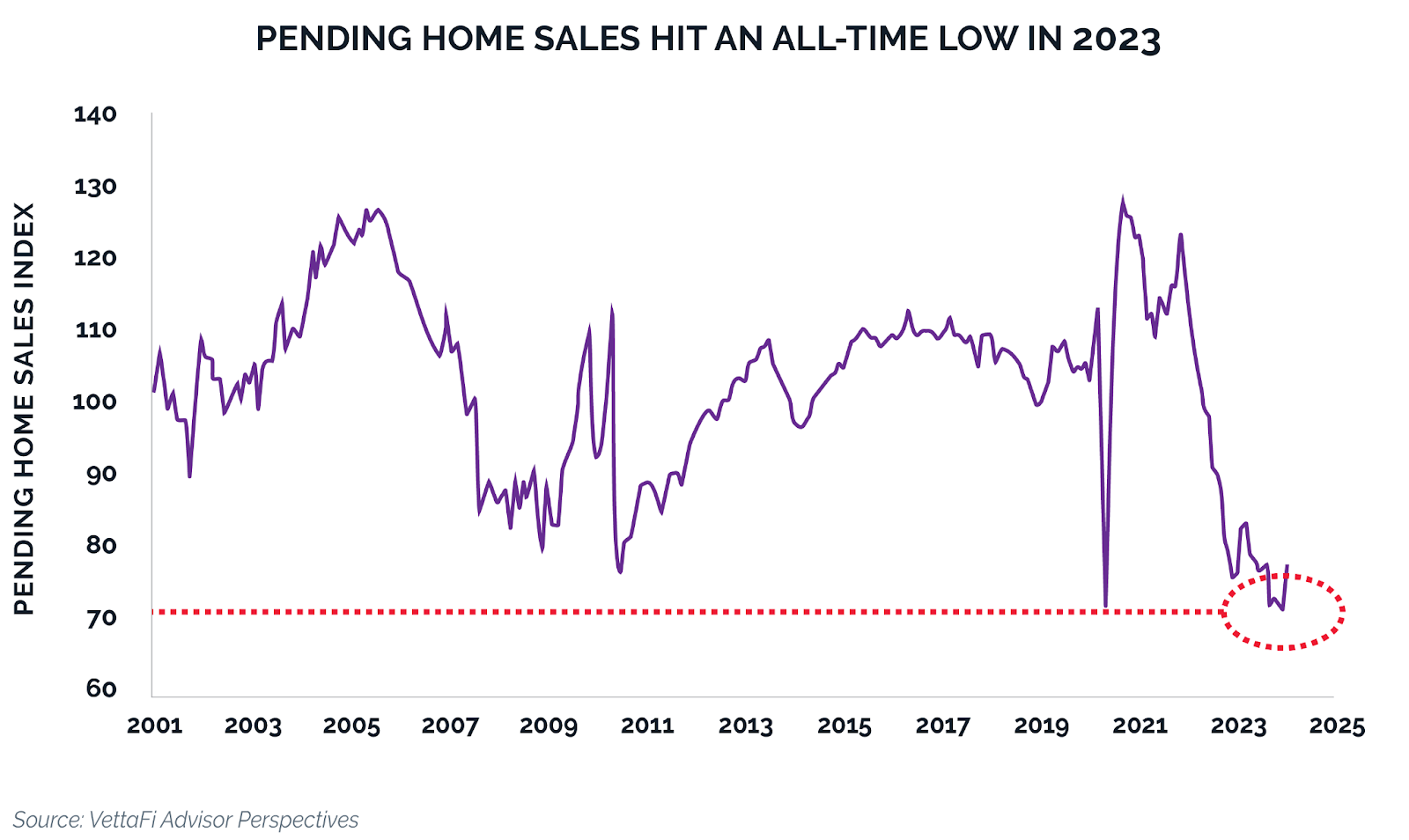

The last four years have been a whirlwind for the storage industry. A rapid acceleration of fundamentals in 2020 and 2021—driven by a considerable increase in demand for storage—was followed by a notably softer 2022 and 2023.

|

On the surface, it would be easy to discount the recent decline in online web rates as purely a function of lower demand, but the story is more complicated than that. Here’s why:

When you go online to rent a storage unit, there are two rates that you see on the website: the ‘web rate’ and the ‘in-store’ rate. Historically, the industry has used the ‘web rate’ as the primary indicator of health. This is the rate that a customer can lock in if they rent online. When developing storage, web rates have been used in modeling assumptions regarding what rates we expect to achieve out of the gate when leasing a store.

|

This can’t be done anymore.

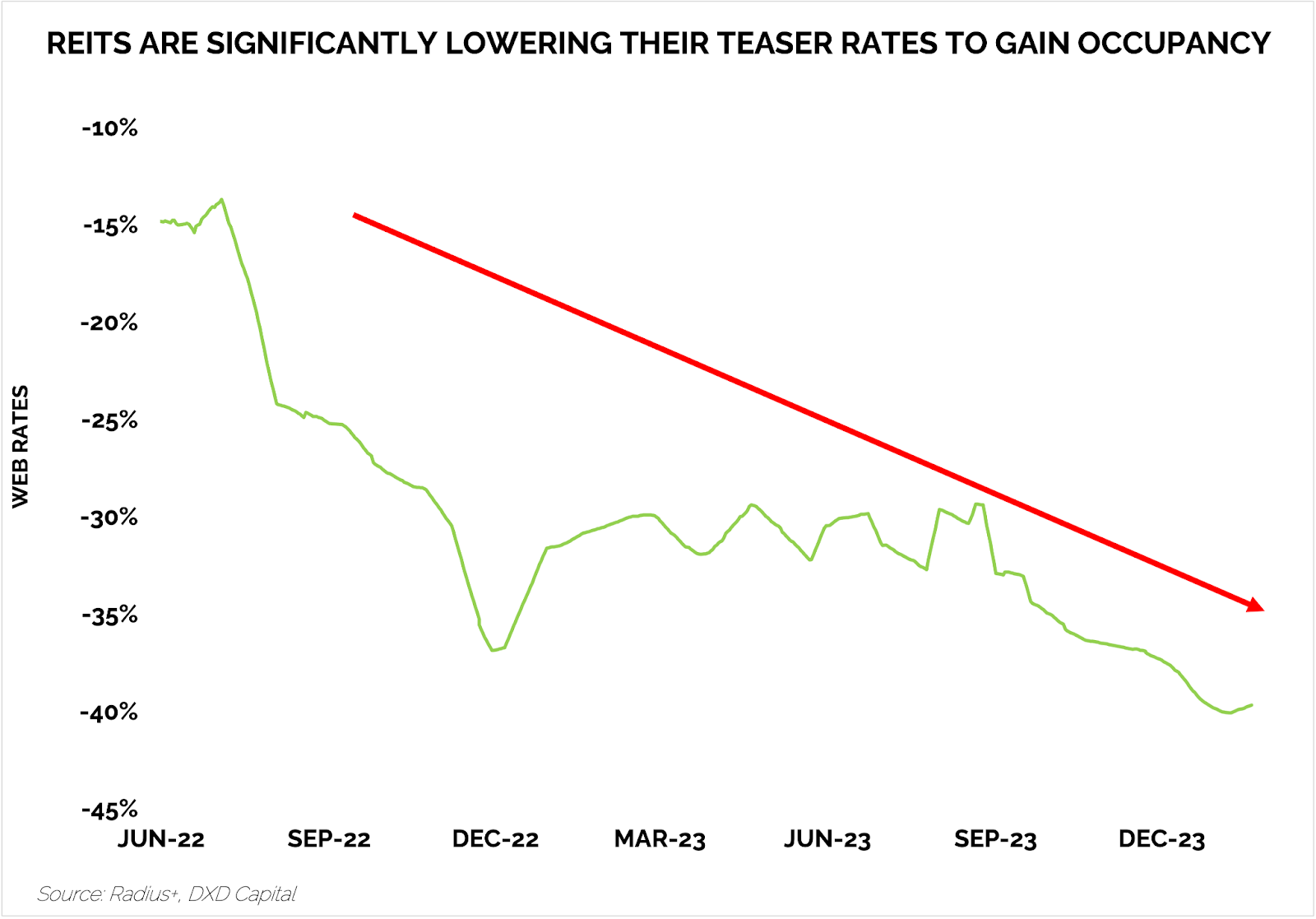

The REITs are slashing their web/teaser rates to gain occupancy and dramatically increase those rents after a very short period of time.

|

What does this mean for developers?

If developers continue to use only web rates in their underwriting models, most development opportunities would no longer hit the required return thresholds.

After discussing the change in methodology, we are now using other data to underwrite our models - with the goal being to use something that reflects the actual rate that most customers are paying after a few months.

Most developers will overlook this nuance, and these lower web will continue to hinder development activity, which, all things being equal, will restrain new storage supply, at least in the near term.

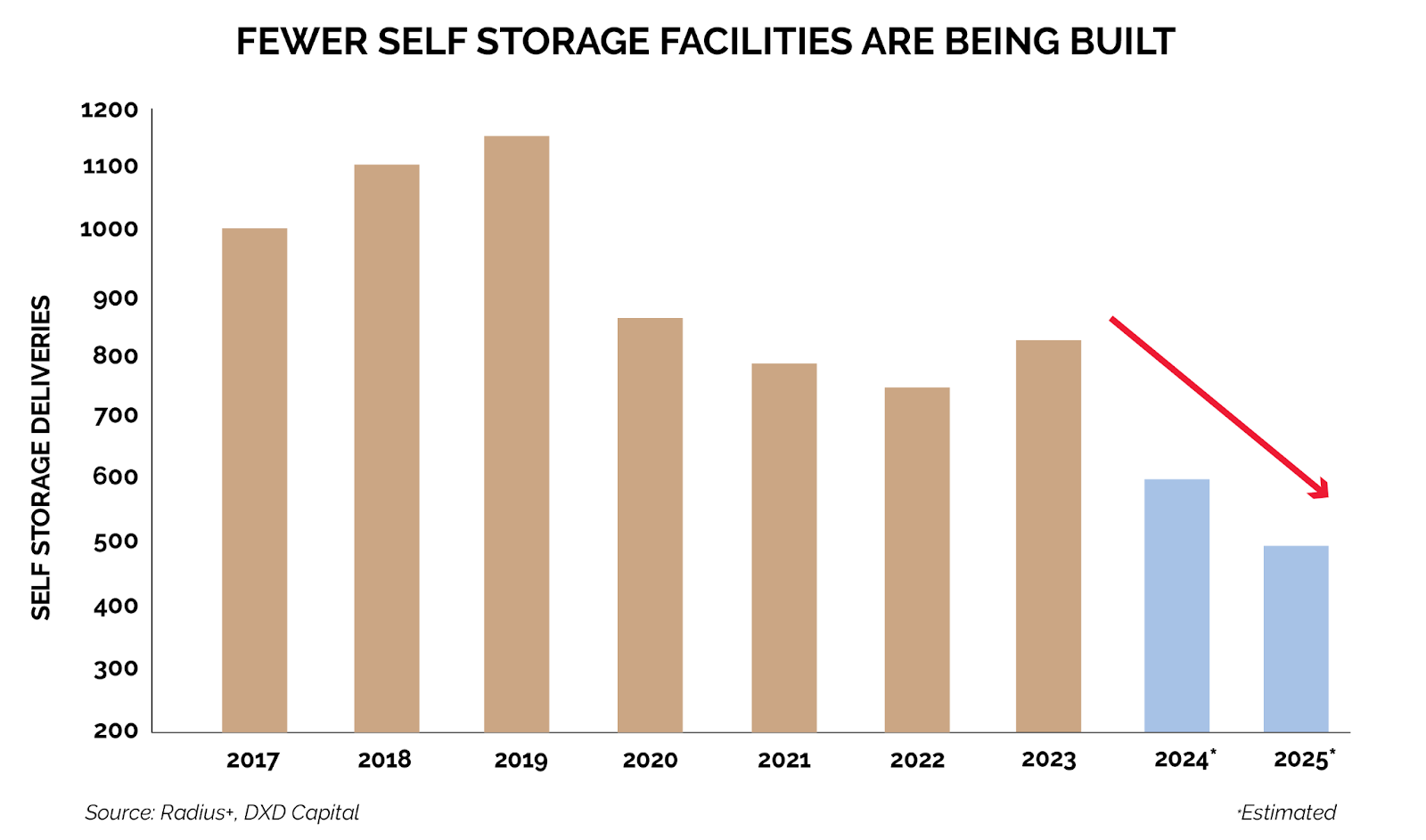

Where is supply going?

The short answer is it will be significantly lower over the next several years than it has been since I entered the industry in 2015.

|

The reasons for the lower supply are threefold:

- The teaser rate dynamic (as discussed above).

- Equity has been challenging to source for new projects since the middle of 2022 and that continues to be the case today.

- Banks are still on the sidelines as they have had various issues with their balance sheets.

Digging a little deeper:

At the end of 2022, the capital markets stopped underwriting new deals. The uncertainty created by dramatically higher interest rates, along with fears of a worn-out consumer and slowing economic activity, were enough to pause new investment.

Institutional equity, which enables most storage development activity, put pencils down in September of 2022; they are largely still on the sidelines.

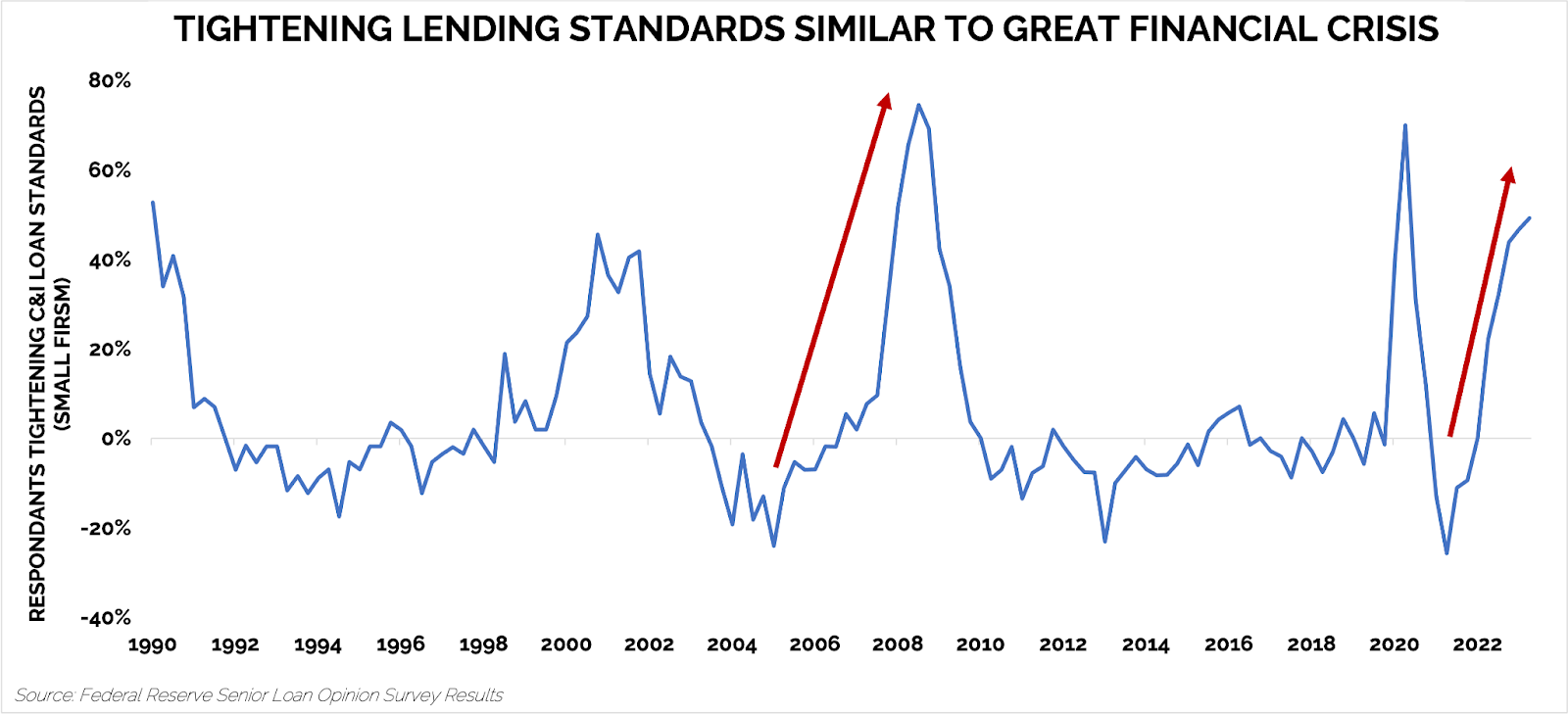

Banks have had their own unique set of challenges as well.

The velocity of interest rate increases, coupled with a structural shift in the office market and oversupply in the multifamily sector, created havoc for bank balance sheets. Regional banks, the lending lifeblood for storage development, have seen significant outflows in bank deposits, reducing their ability and willingness to make new loans.

Data from the Federal Reserve shows the results of regular bank surveys they conduct. As you can see, the recent pace of tightening resembles that of the last financial crisis in 2009.

|

In spite of those headwinds, DXD has continued to find ways to leverage new and existing lending relationships to get projects funded. We are comfortable saying that DXD is in the minority of groups that have been successful in this realm. As evidence of this, we have been inundated with other developers sending us shovel-ready projects where they are unable to source debt and/or equity.

Self storage demand

We discussed how the recent drop in ‘teaser rates’ is partially due to a change in revenue management techniques by the REITs. The other dynamic at play is softer underlying demand for storage.

What has caused this?

Fewer people have been moving over the last 24 months than at any time over the last 40 years.

|

Why are fewer people moving?

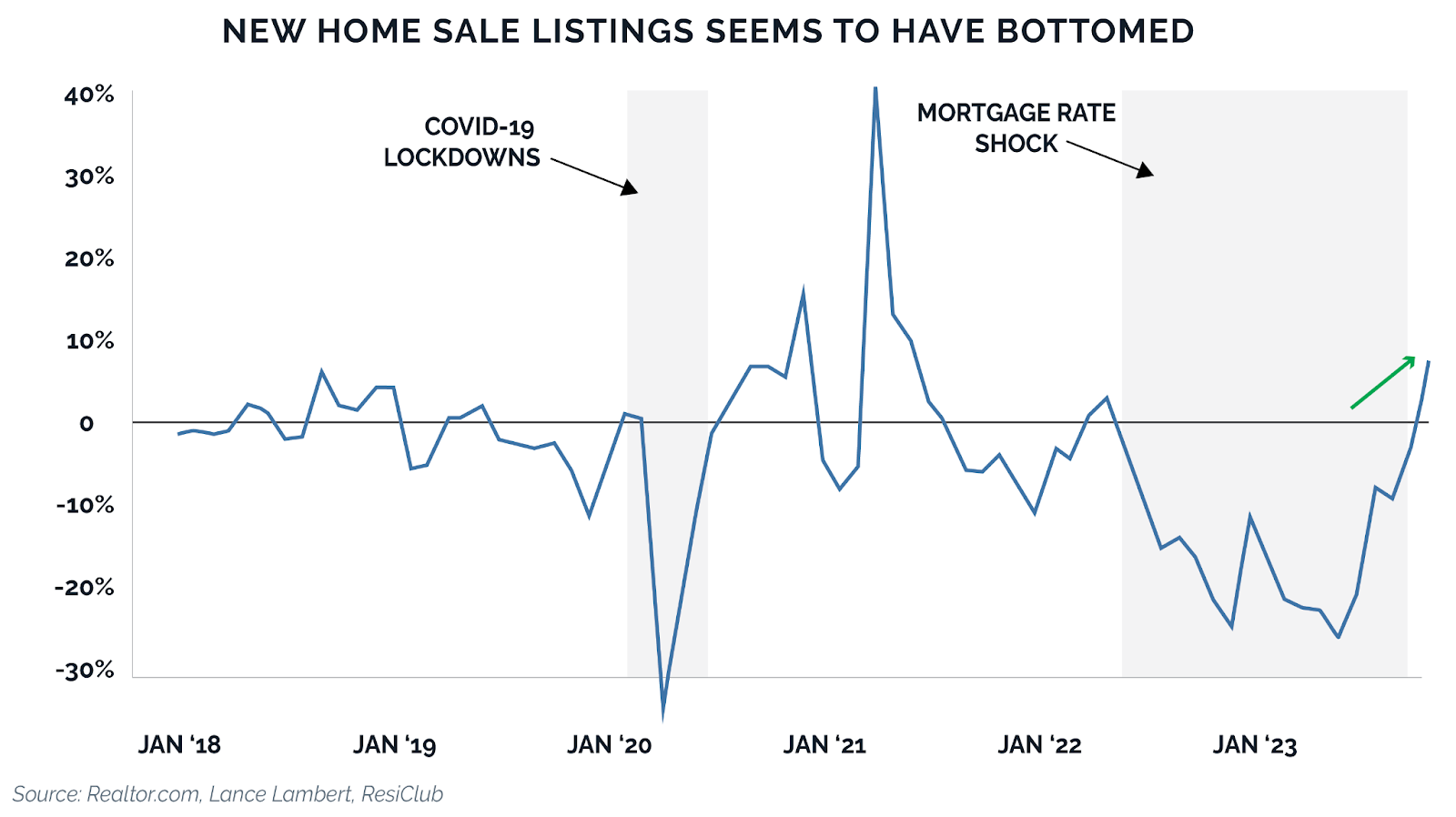

The rapid increase in mortgage rates over the last 24 months created a dynamic the industry refers to as the “lock-in effect.”

Mortgage rates went from three percent in 2021 to above eight percent in 2023. As a result, there has been a drastic decrease in the number of would-be sellers; instead, homeowners are opting to stay put with lower rates/monthly payments vs. moving and taking on a much more expensive mortgage.

The chart below shows the change in new home sales listings - as you can see from the gray-shaded period labeled “mortgage rate shock,” there has been a dramatic pullback in the number of homes for sale.

|

Fewer homes for sale leads to fewer home purchases. In turn, fewer people are moving, which is a notable demand driver for storage. This has been an enormous drag on total storage demand. We estimate that total storage demand in 2023 was 15% lower just from this factor.

Where does it go from here?

Absent a dramatic resurgence in inflation, the Federal Reserve has indicated interest rates have peaked, which is already translating into lower mortgage rates. While the pace of the mortgage rate decline is anyone's guess, it is our view that the decline in home sales has bottomed out. Said differently, in 2023, home sales were a drag on storage demand; in 2024, it will be a tailwind.

Construction costs

One of the largest variables that determines a project's feasibility is the cost to build it.

Construction costs have risen dramatically since 2020 but have remained stable for the past 18 months. We continue to ask ourselves when (or if) they will come down. All things being equal, they ‘should’ as all major commercial real estate asset classes have essentially stopped planning new development projects.

Why might they not come down?

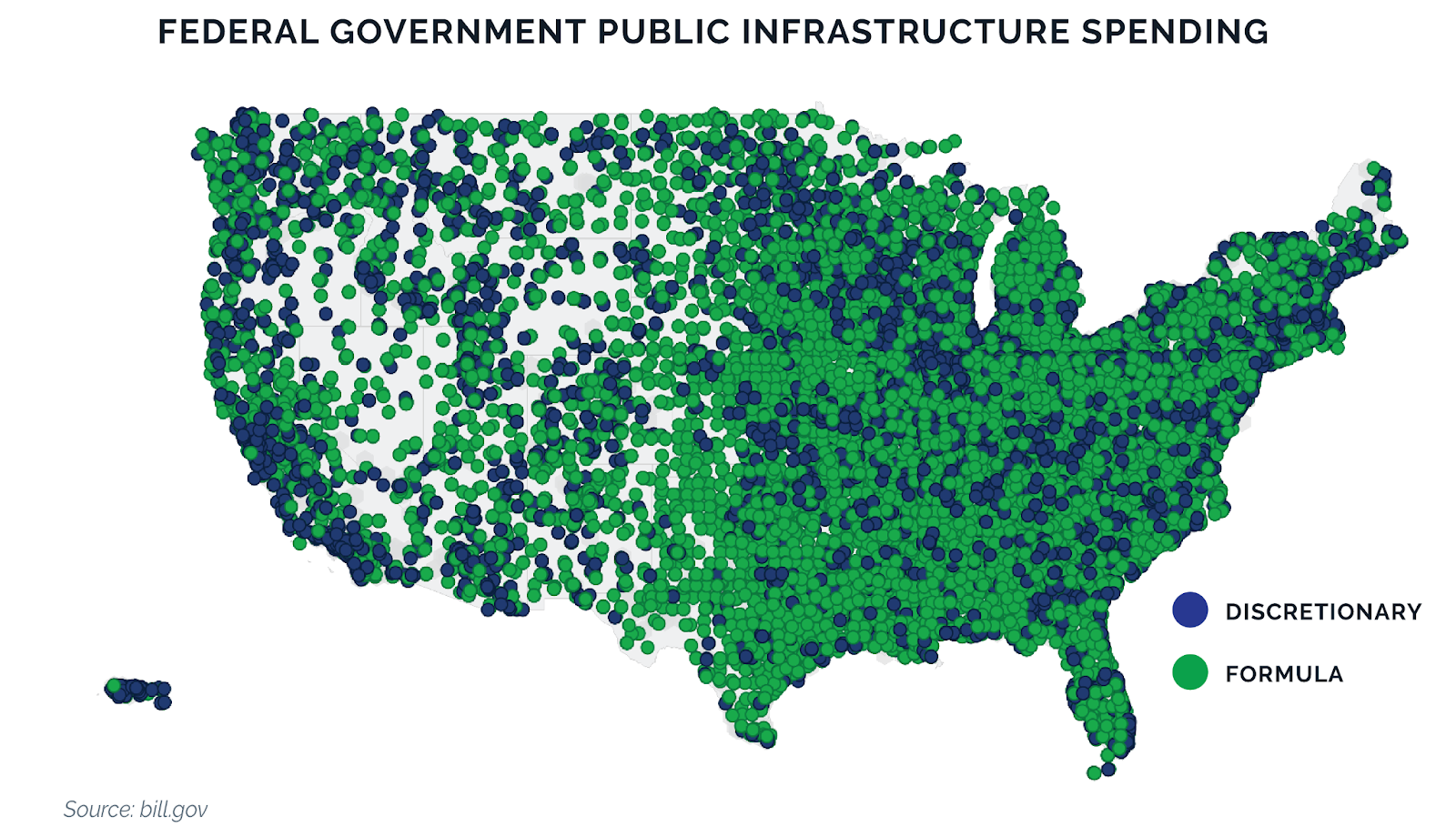

The federal government.

At the end of 2021, the federal government passed the Infrastructure Investment and Jobs Act, a $1.2 trillion bill that authorized $550 billion in new infrastructure projects. The map below shows the magnitude of the various projects underway nationwide.

|

Some contractors used to have 70% of their business from the private sector and 30% from the government; many now have the opposite. The impact of this government spending on the materials and labor market will, at minimum, make any declines in construction costs less than they would have been otherwise; in the worst case, we won’t see any declines.

While we are finding projects that can sustain current construction costs, a 10-15% reduction would dramatically increase returns. While we hope this will happen, we aren’t counting on it.

Putting this all together

As I write this today, our development pipeline has never been larger. We have new opportunities under contract from Maui to Nantucket. Our strategy of focusing on building technology and a team to be able to analyze more opportunities than anyone has ever done before is working.

That said, we also see an incredible opportunity to start acquiring recently built and/or mismanaged storage assets across the country. With the change in interest rates and lending availability, many developers and operators will be looking for an off-ramp as they will not be able to achieve their original objectives. We acquired our first seven-asset portfolio last month, which is just the first of many fantastic opportunities coming to the market.

I’m looking forward to a very exciting 2024.

If you have an interest in learning more about deals we are pursuing at DXD Capital, feel free to reply to this email or click here and we would be happy to discuss.

Cory

Co-Founder DXD Capital, Radius+, ManageSpace

Cory Sylvester

Documenting my journey operating a $500 million self storage portfolio & running multiple real estate, and real estate technology companies with 60 employees.

Last quarter, I highlighted that the commentary out of the major self storage REITs was that pricing power had found stable ground. So what did the REITs say this quarter? Well, more of the same, pricing has indeed bottomed, and they are seeing web rates going positive for the first time in several years. Source: Company Financials, DXD Capital While the road to recovery remains gradual, positive new customer rate trends, stable occupancy, and expanding ancillary income streams all point to a...

Off went the starting pistol, and 115 runners sprinted ahead, jockeying for position. The first 6 miles of the race was straight uphill, and we had 100 miles to go. I was baffled. We would be running for over 24 hours straight—and 60 seconds into the race, I was in last place. I stuck to my guns and ran my race. I walked the first uphill miles, ran when the course turned flat or downhill, and then went back to walking every time the terrain gained elevation. After 31 hours and 15,500 feet of...

I started DXD with the idea that if we could find areas with high rental rates, we could build the most valuable storage properties in the country. Was I right? Yes, and no. Two of DXD’s first projects used this technology, which quickly led us to areas with high rates. That was only part of the equation. We then had to analyze the target and secure parcels zoned for self-storage. At scale, the heatmap rental rate technology increases our efficiency by ~10%-20%. I discovered that the real...