Documenting my journey operating a $500 million self storage portfolio & running multiple real estate, and real estate technology companies with 60 employees.

Why the run-up in residential home prices ends differently this time

Last week's note discussed the reasons behind the near-term slowdown in demand for storage.

This week, we’re zooming out to look at the implications of the housing market as a whole on the storage industry. One place to start our analysis is the last major housing bubble.

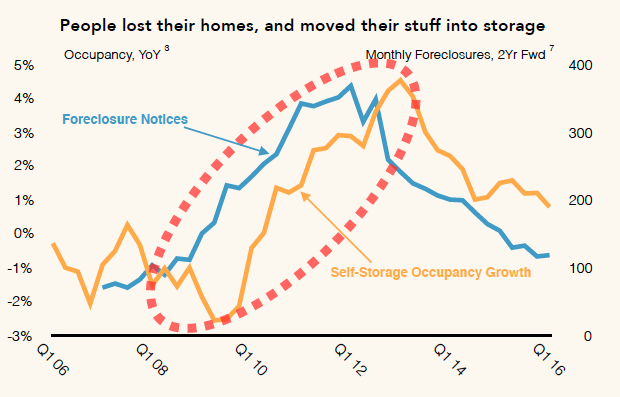

To rewind quickly, during the Great Financial Crisis of 2009 (GFC), there was a large increase in storage demand generated by housing foreclosures:

|

Very simply, if the bubble in the housing market leads to a similar outcome, while it would be painful for the economy, it could have positive implications for storage demand. But will things play out the same or differently this time? I’ve spent some time digging into the housing market to formulate a view of what I think will play out.

Here’s what I found:

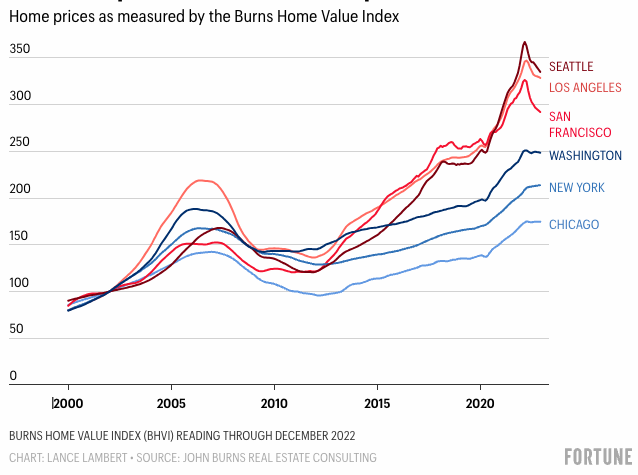

On the surface, it would appear that the housing market bubble is larger than ever before and, all else being equal, a major correction is imminent:

|

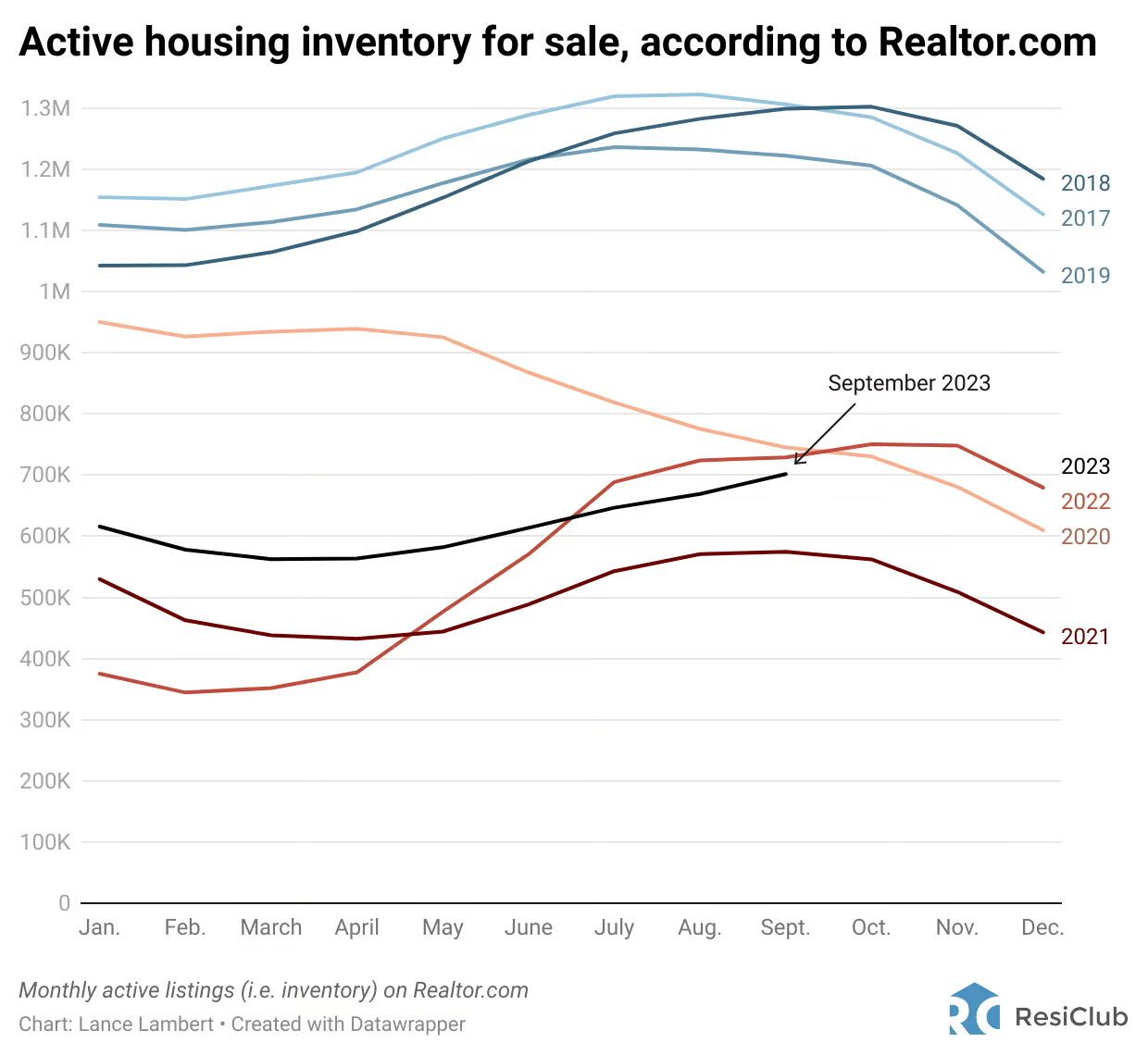

However, there is a major difference between today’s market conditions and those in 2008-2010; in one word: supply. Although home prices (and mortgage rates) are extremely high, the supply of homes available for sale is still very low across the country (~40% lower than pre-COVID levels):

|

With those supply restrictions, a market correction isn’t as imminent as it might first appear. Unlike the GFC, today’s housing market is held in balance by opposing supply and demand constraints. Demand is constrained as existing homeowners are “locked” into low rates and new buyers are priced out of the market by interest rates. Supply is also constrained by those same existing homeowners’ reluctance to trade up to a 7% interest rate.

The net result is that we should have a soft landing in the housing market and should not expect the same or even similar market outcomes as we experienced during the GFC.

The eventual reduction in interest rates should keep these two market forces in balance while simultaneously providing a tailwind to the self-storage industry. As rates decrease, storage demand will rebound as buying and moving activity accelerates, and the market returns to normalcy.

Cory

Co-Founder DXD Capital, Radius+, ManageSpace

Cory Sylvester

Documenting my journey operating a $500 million self storage portfolio & running multiple real estate, and real estate technology companies with 60 employees.

Last quarter, I highlighted that the commentary out of the major self storage REITs was that pricing power had found stable ground. So what did the REITs say this quarter? Well, more of the same, pricing has indeed bottomed, and they are seeing web rates going positive for the first time in several years. Source: Company Financials, DXD Capital While the road to recovery remains gradual, positive new customer rate trends, stable occupancy, and expanding ancillary income streams all point to a...

Off went the starting pistol, and 115 runners sprinted ahead, jockeying for position. The first 6 miles of the race was straight uphill, and we had 100 miles to go. I was baffled. We would be running for over 24 hours straight—and 60 seconds into the race, I was in last place. I stuck to my guns and ran my race. I walked the first uphill miles, ran when the course turned flat or downhill, and then went back to walking every time the terrain gained elevation. After 31 hours and 15,500 feet of...

I started DXD with the idea that if we could find areas with high rental rates, we could build the most valuable storage properties in the country. Was I right? Yes, and no. Two of DXD’s first projects used this technology, which quickly led us to areas with high rates. That was only part of the equation. We then had to analyze the target and secure parcels zoned for self-storage. At scale, the heatmap rental rate technology increases our efficiency by ~10%-20%. I discovered that the real...